Editor's note: This column is part of a series featuring Lakeshore experts offering advice to small businesses as they navigate their recovery through the COVID-19 crisis.

No employees? No problem.

If you are a sole proprietor, LLC with no employees, independent contractor, or otherwise self-employed, you can still get financial help from programs designated in the CARES Act.

As a sole proprietor or business owner, you can apply for and receive a Paycheck Protection Program (PPP) Loan. The great thing about this loan is that if you use 75% of the loan proceeds on payroll (aka paying yourself), and the other 25% on working capital expenses like business leases, utilities, or mortgage expenses, you can have it 100% forgiven.

![]()

This loan is administered through lending institutions. To apply for the PPP, we recommend reaching out to the bank or credit union where you have a relationship first. If you are unable to apply with your current bank, reach out to the community banks in your city, or check out online lenders such as

PayPal,

Fundera, Square, Lendio,

Kabbage,

BlueVine, and others.

The maximum amount you can borrow on the PPP Loan is 2.5x your average monthly payroll (based on 2019 numbers). Since you don’t have employees, you won’t be reporting your payroll costs for the PPP loan. Instead, you’ll be reporting your net business income, which will be reported on a

Schedule C. As long as your business was operational prior to February 15 of this year, you can apply to the Paycheck Protection Program.

According to the U.S. Treasury, “regardless of whether you have filed a 2019 tax return with the IRS, you must provide the 2019 Form 1040 Schedule C with your PPP loan application.” If 2019 Schedule C income is $0 or less, a proprietor without employees is not eligible for a PPP loan. Independent Contractors will need to submit form 1099-MISC in addition to their Schedule C.

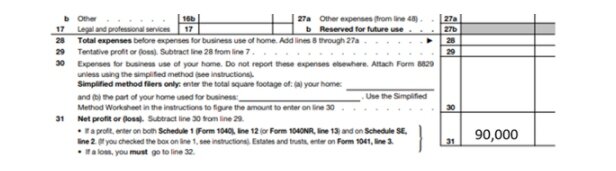

In order to determine the amount of your PPP loan, you will take the amount in line 31 on your Schedule C, Net Profit or Loss (up to a maximum of $100,000), then divide by 12 to come up with your average monthly profit. You then multiply that amount by 2.5 to come up with your loan amount.

![]()

Let’s say Line 31 is $90,000.

Net Profit: $90,000

Average Monthly: $90,000/12 = $7,500

Amount of PPP: $7,500 x 2.5 = $18,750

To get 100% forgiveness:

Pay back 75% on payroll costs: $14,063.50 over eight weeks.

Other 25% can be used for lease, utilities, mortgage expense: $4,687.50

![]() Pandemic Unemployment Assistance (PUA)

Pandemic Unemployment Assistance (PUA)

With Pandemic Unemployment Assistance (PUA), many people, including those who don’t typically qualify for unemployment benefits, including self-employed individuals, may qualify for PUA. Under PUA, Individuals will receive an established weekly benefit amount and an additional $600 per week in Pandemic Unemployment Compensation.

In the state of Michigan, the minimum unemployment benefit is $162/week and the maximum is $362/week. Depending on your earning history, you would be eligible for the Michigan benefit plus the federal amount of $600.

You do not need to show proof of earning to apply for and receive unemployment benefits. If you do not supply additional information, you will automatically be given the lowest rate of $162 + $600 or $762/week.

If you can show proof of earnings (see below), you can get as much (depending on earnings as $362 + $600 or $962/week.

PPP or PUA?

Since both the PPP and PUA are meant to replace your earnings, you can’t get both. So which one is best for you? As always, the answer is “it depends.” You should run scenarios with both, taking into consideration how long you think it will be before you are back up to speed with your business. The PPP covers eight weeks, the PUA currently is in effect until July 31.

![]()

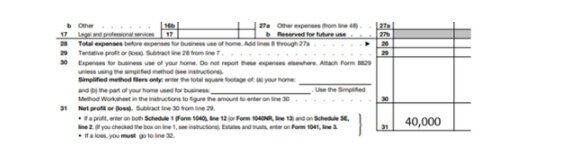

Net Profit: $40,000

Average Monthly: $40,000/12 = $3,333

Amount of PPP: $3,333 x 2.5 = $8,333

Unemployment

Weekly amount: $962 x 16 weeks = $15,392

In this example, the PPP would generate $3,333/month of forgivable expenses, where unemployment would be $3,848 for four weeks. Additionally, if needed it could be extended through July 31. So, in this case, it would be better for you to apply for unemployment.

Every case is different so you will need to do the analysis for your particular business. If you need help navigating this or other COVID-19 relief programs, SBDC consultants are here to assist you!

Register for our no-cost consulting services.

Liz Hoffswell is a certified business consultant for the Michigan Small Business Development Center, which is based at the GVSU Seidman School of Business in Grand Rapids. She has more than 25 years of experience in management, operations, finance, sales, and marketing, working with organizations of all sizes. Additionally, Hoffswell is a serial entrepreneur and has started several small businesses throughout her career.

If you have a topic or question you would like Liz to address, send an email to Managing Editor Shandra Martinez at shandra@issuemediagroup.com.

This article is part of The Lakeshore, a new featured section of Rapid Growth focused on West Michigan's Lakeshore region. Over the coming months, Rapid Growth will be expanding to cover the complex challenges in this community by focusing on the organizations, projects, programs, and individuals working to improve conditions and solve problems for their region. As the coverage continues, look for The Lakeshore publication, coming in 2020.